China Online Market Analysis: Digital Marketing Trends and Consumer Behavior Insights

- On July 7, 2025

- china customer behavior, china market trends

I. Executive Summary

This report provides a comprehensive analysis of China’s online market, highlighting its immense scale and rapid evolution. The digital advertising market is projected to reach US145.39 billion by 2030,while digital media is expected to hit US236.78 billion by the same year, driven by robust compound annual growth rates. Social commerce, a particularly dynamic sector, is forecasted to achieve a staggering US$8.55 trillion by 2033, with China commanding half of the global market share in 2024. This digital transformation is underpinned by over a billion mobile internet users, establishing a “mobile-first” imperative for marketers.

Key digital marketing trends include the dominance of smartphone-based advertising and the burgeoning growth of video and interactive media. Social commerce and live streaming are pivotal, with Douyin’s e-commerce Gross Merchandise Volume (GMV) reaching approximately 3.5 trillion yuan in 2024, demonstrating a strategic shift towards shelf-based shopping and merchant self-broadcasts. Artificial intelligence (AI) is emerging as a critical efficiency multiplier, with its adoption poised for significant growth, especially as domestic innovations like DeepSeek AI drive down costs and democratize access to advanced capabilities. Analysis of marketing investments reveals the enduring value of traditional media alongside digital channels, underscoring the necessity of integrated strategies for optimal return on investment.

Consumer behavior in China is undergoing nuanced shifts, characterized by a post-pandemic move towards purpose-driven consumption, a heightened demand for convenience, and a strong preference for quality, durability, and transparent processes. Omnichannel shopping is now the norm, with a substantial 85% of consumers preferring a blend of physical and digital platforms, and instant retail rapidly expanding to meet immediate needs. Generational differences are pronounced: Gen Z, despite lower disposable incomes, prioritizes emotional fulfillment and unique offerings, while the rapidly growing “silver economy” demonstrates increasing digital engagement but maintains a cautious, value-driven approach to spending, often influenced by younger family members.

Navigating China’s complex regulatory landscape, particularly concerning data security and content censorship, remains paramount for businesses. The “1+N” policy framework for the digital economy and the extraterritorial reach of laws like the Anti-Unfair Competition Law necessitate a deep understanding of local compliance requirements. Success in this unique market hinges on strategic adaptation, cultural localization, and a holistic approach that integrates advanced digital capabilities with a profound understanding of evolving consumer preferences and regulatory nuances.

II. Introduction: China’s Digital Landscape Overview

Defining the Scope: Digital Marketing, Consumer Behavior, and Key Market Segments

This report meticulously examines the intricate interplay between digital marketing strategies and the evolving consumer behaviors within China’s dynamic online ecosystem. The analysis encompasses key market segments that collectively define the digital landscape: digital advertising, which includes various online promotional activities; digital media, covering content consumption across platforms; social commerce, a rapidly expanding sector integrating social interaction with e-commerce; the broader e-commerce market, encompassing online retail transactions; and instant retail, a burgeoning segment focused on rapid delivery of goods. By focusing on these interconnected areas, the report aims to provide a comprehensive understanding of the forces shaping China’s digital economy.

Significance of the Chinese Market in the Global Digital Economy

China’s digital economy holds an undeniably pivotal position on the global stage, distinguished by its sheer scale, rapid innovation, and unique market characteristics. The nation’s digital prowess is evident in its significant contribution to global digital markets. In 2024, China accounted for a substantial 11.0% of the global digital advertising market , underscoring its role as a major player in online promotions. Similarly, in 2023, it represented 11.7% of the global digital media market, indicating its vast consumption and production of digital content. Perhaps most strikingly, China dominated the social commerce sector, holding an impressive 50.0% of the global market share in 2024. This commanding presence highlights the country’s pioneering role in integrating social interactions with commercial transactions.

This robust digital transformation is fundamentally underpinned by widespread mobile internet adoption. China boasts over 1 billion mobile internet users, with penetration rates surpassing 99% in urban areas, making mobile platforms the primary gateway to the digital world for the vast majority of the population. The market is currently navigating a “new reality” characterized by resilient, albeit modest, single-digit consumption growth. This indicates a maturing yet highly dynamic environment where growth continues, but with a greater emphasis on quality and value rather than sheer volume. This context establishes China not merely as a large market, but as an indispensable and complex environment demanding tailored strategies for global businesses seeking to thrive.

III. Digital Marketing Trends and Market Dynamics

A. Market Size and Growth Projections

The Chinese online market is characterized by robust growth across its various digital segments, presenting significant opportunities for businesses.

Digital Advertising Market Outlook (2024-2030): The digital advertising market in China is on a strong upward trajectory. In 2024, the market revenue stood at US53,438.5 million. Projections indicate a substantial expansion, with the market expected to reach an estimated revenue of US145,389.8 million by 2030. This growth translates to a Compound Annual Growth Rate (CAGR) of 18% from 2025 to 2030, signaling a highly dynamic and expanding sector for online promotions.

Digital Media Market Outlook (2024-2030): Complementing the advertising sector, the digital media market in China is also poised for significant growth. With a market revenue of US109,060.1 million in 2024, it is for ecasted to reach US236,781.5 million by 2030. This represents a healthy CAGR of 13.8% from 2025 to 2030, indicating increasing consumption and monetization of digital content across various platforms.

Social Commerce Market Growth (2024-2033): The social commerce sector in China exhibits particularly explosive potential. Starting from a revenue of US579,635.9 millionin 2024, it is projected to reach a staggering US8,546,794.9 million by 2033. This remarkable expansion is driven by an impressive 35.8% CAGR from 2025 to 2033. China’s dominant position in this segment is clear, as it accounted for half of the global social commerce market in 2024, highlighting its pioneering role in integrating social interaction with commercial transactions.

E-commerce Market Overview (2023-2035): The broader e-commerce market in China, a foundational pillar of its digital economy, was valued at US764.53 billionin 2023 and grew to US888.39 billion in 2024. This market is projected to expand significantly to US$7,449.78 billion by 2035, demonstrating a robust 21.327% CAGR from 2025 to 2035. This expansion is largely fueled by China’s extensive mobile internet penetration, with over 1 billion smartphone users, and a steady increase in disposable incomes among its population.

Instant Retail Market Growth (2023-2030): Instant retail is rapidly reshaping China’s consumption landscape, offering unparalleled convenience. The market reached 650 billion yuan ($89 billion) in 2023, marking a significant 28.89% year-on-year increase, far outpacing the 11% rise in online retail sales. Projections from the Chinese Academy of International Trade and Economic Cooperation indicate that this sector will surpass 2 trillion yuan ($274 billion) by 2030. Major players illustrate this momentum: Meituan, a leading on-demand service platform, recorded a new daily order record of 120 million across its instant retail services on July 5. JD.com’s “Seconds Delivery” service also demonstrated remarkable growth, exceeding 10 million daily orders across 166 cities. Even short-video platform Douyin has entered this space, with its instant retail gross merchandise volume (GMV) growing by over 50% in 2024. This rapid expansion signifies a profound shift in consumer expectations toward immediate gratification and on-demand delivery.

B. Key Digital Advertising and Media Segments

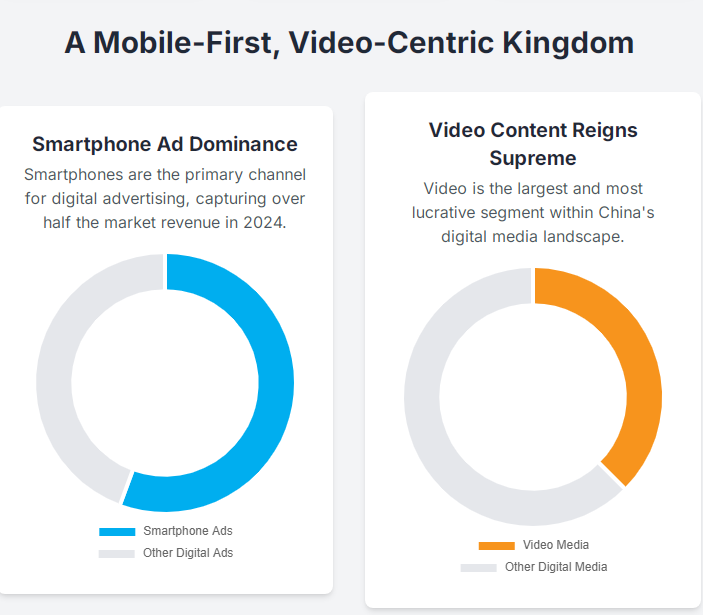

Dominance of Smartphone in Digital Advertising: Smartphones are the undisputed leaders in China’s digital advertising market, serving as the primary device for consumer engagement. In 2024, smartphones constituted the largest revenue-generating component, capturing a commanding 55.63% share of the digital advertising market. This segment is also projected to exhibit the fastest growth during the forecast period. This overwhelming dominance is directly attributable to China’s rapid mobile internet expansion, which has resulted in over 1 billion mobile internet users. Consequently, mobile platforms such as WeChat and Douyin have become indispensable for advertisers aiming to influence a wide audience across the region, necessitating mobile-first strategies for effective reach and engagement.

Growth in Video and Interactive Media: Within the broader digital media market, video content has emerged as the most significant revenue-generating type. In 2023, video held the largest share, and by 2024, it accounted for 37.51% of the market. Beyond passive video consumption, interactive media is identified as the most lucrative content type segment, poised for the fastest growth during the forecast period. This trend is further amplified by the rapid expansion of live streaming commerce, which offers an engaging and interactive purchasing experience, particularly appealing to younger consumers and driving significant online engagement and sales. The convergence of video content, interactive elements, and live streaming creates a rich environment for dynamic digital marketing campaigns.

C. Emerging Marketing Channels and Strategies

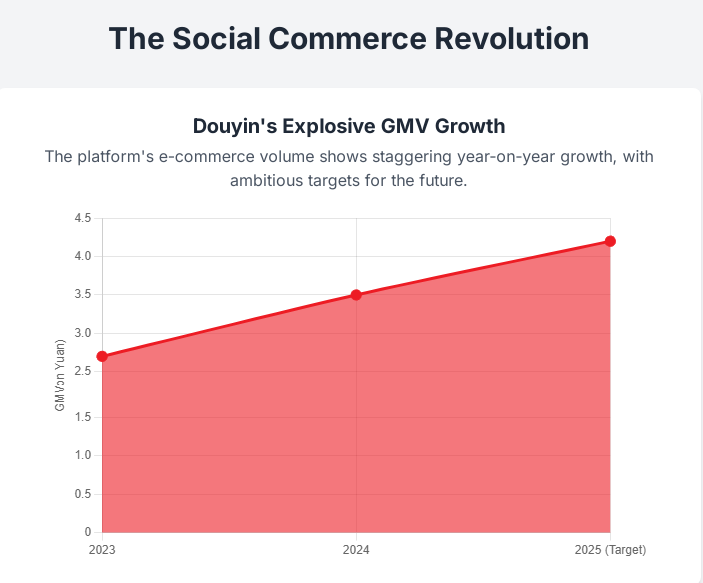

The Rise of Social Commerce and Live Streaming: Social commerce is not merely an emerging trend but a burgeoning force fundamentally reshaping China’s digital marketing landscape. This sector seamlessly integrates social interactions with e-commerce, allowing consumers to discover and purchase products directly within social media environments. A significant 71% of Chinese consumers report discovering new products on social media platforms, and over 50% proceed to make purchases directly via live streams. Douyin E-commerce serves as a prime example of this phenomenon, with its Gross Merchandise Volume (GMV) experiencing a remarkable 30% year-on-year growth in 2024, reaching approximately 3.5 trillion yuan. The platform has set an ambitious target of 4.2 trillion yuan for 2025, underscoring the explosive potential and strategic importance of this channel.

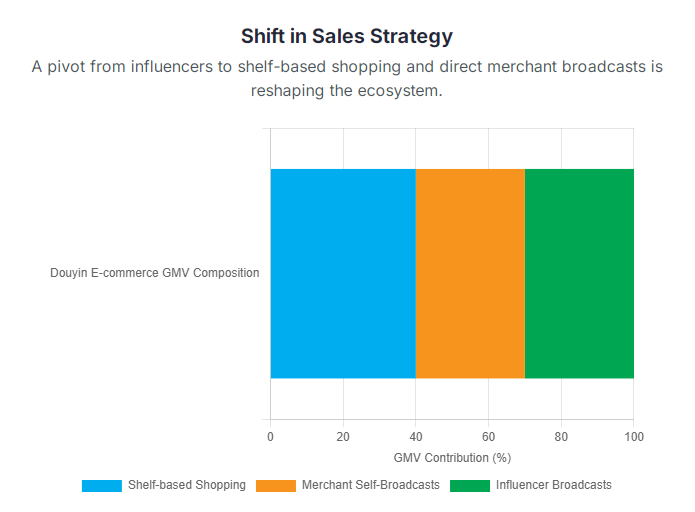

Role of Influencers and Merchant Self-Broadcasts: While influencer live broadcasts have historically been a cornerstone of social commerce, contributing approximately 30% to Douyin’s GMV in 2024, a notable strategic shift is underway. The platform is evolving from a purely discovery-driven, influencer-centric model to a more comprehensive “full-domain interest-based e-commerce” approach. This evolution is evidenced by the increasing prominence of shelf-based shopping, which now accounts for over 40% of Douyin’s GMV. Furthermore, store-hosted live broadcasts, where merchants directly manage their own live-streaming sales, contributed slightly over 30% to the overall GMV, surpassing influencer live broadcasts for two consecutive years. This indicates a growing preference for brands to control their own live-streaming narratives and sales processes, potentially leading to greater cost efficiency and brand consistency. Douyin’s strategic direction for 2025 reflects this pivot, with plans to increase subsidies for shelf-based e-commerce and to focus resources on brand merchants and large non-brand merchants for their self-broadcasts. While supporting small and medium influencers remains part of the strategy, the emphasis is clearly shifting towards empowering merchants directly. This development suggests that for marketers, while influencer collaborations remain relevant, investing in and optimizing their own official stores and conducting regular, high-quality merchant self-broadcasts on platforms like Douyin is becoming increasingly important for sustainable and effective sales channels.

D. AI Integration in Digital Marketing

Current Adoption and Future Potential of AI Marketing: The integration of Artificial Intelligence (AI) into digital marketing practices in China is still in its nascent stages but holds substantial growth potential. According to the 2025 China Digital Marketing Trend Report by Miaozhen Systems, a Beijing-based marketing research company, 54% of advertisers currently report weekly AI usage across their operations. However, the specific application ratio of AI within marketing functions remains relatively low at 28%. This disparity suggests that while businesses are experimenting with AI in broader operational contexts, its full transformative impact on marketing campaigns and strategies is yet to be realized. This indicates a significant untapped potential for AI to revolutionize various aspects of digital marketing in the coming years.

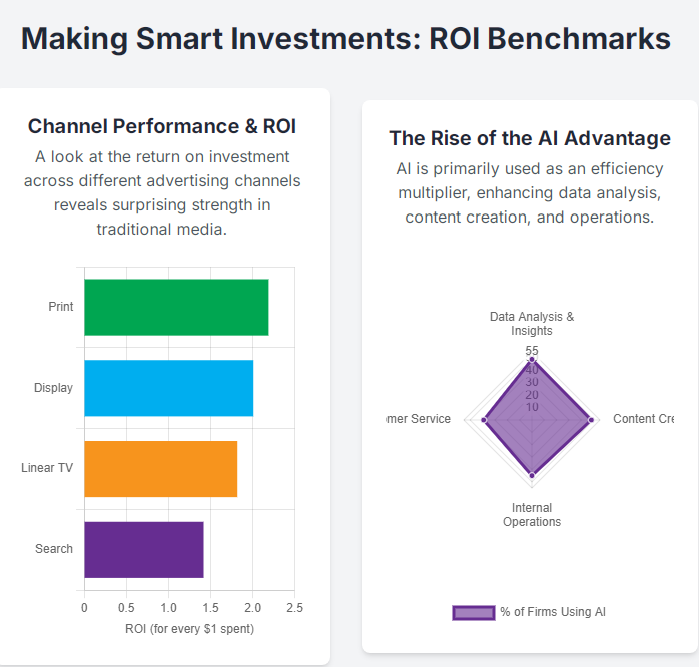

Advertiser Sentiment and Application Scenarios: Advertisers in China are keenly aware of AI’s practical benefits and express a strong intent to leverage it for operational enhancements. A notable 41% of advertisers plan to utilize AI marketing to address critical challenges, including optimizing the efficiency of AI advertisements, intelligent ad placement, deriving deeper user insights, enhancing data analysis capabilities, and streamlining product innovation and distribution processes. This focus on efficiency and data-driven decision-making is corroborated by Huawei’s Q1 2025 Digital Business Index, which illustrates AI’s diverse applications within businesses: 49% of firms use AI for data analysis and insights, 48% for content creation (such as marketing materials and reports), 45% for internal operations (like workflow automation), and 39% for customer service (including chatbots and automated support). These applications highlight AI’s role as an efficiency multiplier, enhancing back-end processes and data-driven decision-making rather than solely focusing on front-end creative campaigns.

DeepSeek AI’s Impact: The emergence of the Chinese AI lab DeepSeek AI in early 2025 marks a pivotal moment in the accessibility and adoption of advanced AI capabilities within China. DeepSeek AI’s cost-efficient, high-performing AI models, such as DeepSeek R1 and DeepSeek-V3, have demonstrated the ability to rival global leaders like OpenAI’s models, but at a fraction of the typical training cost (e.g., an estimated $5.5 million for DeepSeek-V3 compared to $100 million for OpenAI’s GPT-4). This significant cost disruption has already exerted considerable pressure on major Chinese tech giants, including Alibaba, Baidu, and Tencent, compelling them to lower their AI service rates. The consequence of this price war is the democratization of access to sophisticated AI tools, making them more affordable and accessible to a broader range of businesses, including small and medium-sized enterprises. This development is expected to spur wider AI adoption across China, establishing AI-powered optimization as a baseline expectation rather than a premium advantage, and potentially leveling the competitive playing field by making advanced capabilities available to more players.

E. Marketing Investment and ROI Benchmarks

Trends in Marketing Expenditure and Channel Performance: Analysis of marketing investments in China reveals a dynamic landscape where strategic allocation is key to achieving optimal returns. According to Keen’s “2024 Performance Insights & Strategic Investment Guide for 2025,” clients increased their overall marketing investments by 15% in 2024, which corresponded to a 4% rise in Return on Investment (ROI) through data-driven, optimized strategies. Specifically, media spend grew by 16%, resulting in an 8% boost in ROI. Digital channels, particularly Social and Streaming platforms, captured a combined 35% of marketing budgets, reflecting their increasing influence and generally improved profitability. Looking ahead, mobile internet is anticipated to see a significant 55% growth in investment in 2025, underscoring its continued importance as a primary medium for reaching consumers.

Balancing Top-of-Funnel and Bottom-of-Funnel Investments: Marketers in 2024 grappled with the strategic balance between brand-building (top-of-funnel) and immediate performance-driven (bottom-of-funnel) investments. Enterprise brands, those with over $500 million in spend, notably leaned heavily into top-of-funnel efforts, prioritizing brand awareness and long-term value creation. In contrast, mid-market brands adopted a more balanced approach, allocating their spend almost equally, with a 47-53% split between top-of-funnel and bottom-of-funnel tactics. Across all market segments, there was a discernible increase in investments directed towards top-of-funnel activities, signaling a renewed focus on building brand equity and recognition. This suggests that even modest shifts towards brand-building tactics can yield significant long-term brand value in 2025, emphasizing the importance of a holistic marketing approach that nurtures brand perception alongside driving immediate sales.

ROI Benchmarks: The report provides specific ROI benchmarks that challenge conventional assumptions about media effectiveness. Search advertising delivered an ROI of $1.43 for every dollar spent. However, surprisingly, traditional media channels like Linear TV ($1.83 ROI) and Print ($2.20 ROI) demonstrated respectable, and in some cases superior, returns, defying the notion that digital channels invariably outperform traditional ones. Display advertising also showed a strong ROI of $2.02, though its marginal ROI was lower at $0.83. This data indicates that a purely digital-centric approach may not be optimal. Instead, a balanced, multi-channel strategy that leverages the unique strengths of both digital (for precision targeting, engagement, and direct conversion) and traditional media (for broad brand awareness, trust, and credibility) is crucial. The strong performance of traditional media implies that these channels can still be highly effective for reaching specific demographics or for foundational brand-building efforts, especially when integrated with and supported by targeted digital campaigns to maximize overall marketing return.

IV. Evolving Consumer Behavior Insights

A. Shifting Consumption Patterns

Chinese consumer behavior is undergoing a profound transformation, influenced by post-pandemic realities and evolving priorities.

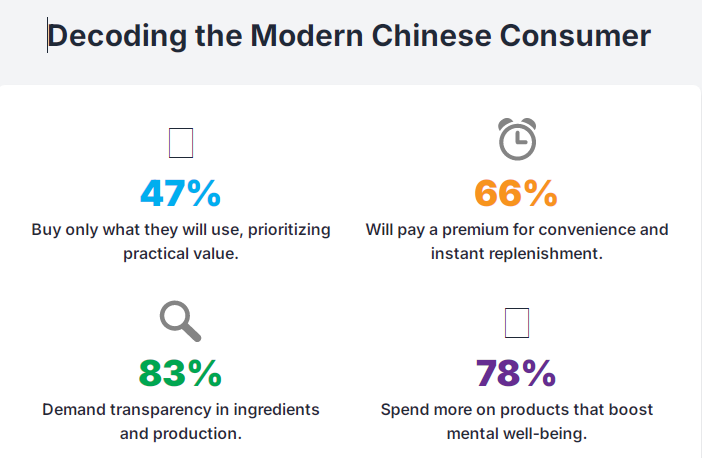

The Era of Purpose-Driven Consumption: In the post-pandemic era, Chinese consumers have adopted a more cautious, value-oriented, and strategic approach to their spending habits. A significant finding from recent surveys indicates that 47% of Chinese consumers now exclusively purchase products they know they will use, actively endeavoring to avoid unnecessary waste. This shift is largely influenced by prevailing economic uncertainties, with 31% of consumers expressing concern about potential economic downturns, and 29% worrying about their family’s overall well-being and happiness. These concerns have led to a more deliberate approach to spending, where essential goods and services are prioritized over discretionary purchases, reflecting a desire for financial security and practical value.

Prioritization of Convenience and Immediate Replenishment: A strong and accelerating demand for convenience characterizes current Chinese consumer behavior. A notable 66% of Chinese consumers express a willingness to increase spending on convenience-related products and services, a figure that is 4 percentage points higher than the Asia-Pacific average. This preference is particularly evident among smaller household structures, which are increasingly moving away from traditional “bulk purchases and stockpiling” in favor of “on-demand replenishment to avoid waste” and the “purchase of smaller packages”. The proportion of consumers who choose “immediate replenishment without waiting for discounts” has risen to 29%, marking a 9% increase from the previous year, highlighting a growing expectation for instant gratification and efficient fulfillment.

Demand for Quality, Durability, and Transparent Processes: Chinese consumers are becoming increasingly discerning, demonstrating a clear willingness to pay a premium for products that offer superior quality, enhanced durability, and greater functionality. Research indicates that 75% of consumers are prepared to spend more on products with longer lifespans, while an even higher 83% prefer items with transparent ingredient lists and production processes. This emphasis on quality and transparency is particularly pronounced in health and wellness categories, where products offering anti-aging benefits, high efficacy, and energy efficiency are experiencing robust demand, reflecting a growing consumer focus on personal well-being and product integrity.

Focus on Self-Care and Emotional Fulfillment: A significant and growing trend among Chinese consumers is the prioritization of self-care and emotional well-being. A substantial 78% of consumers are willing to allocate more spending towards products that enhance their mental well-being, and 75% are actively investing in vitamins and supplements to boost their physical health. This holistic focus drives demand for products that offer relaxation, comfort, and sensory pleasure, reflecting a broader societal shift towards seeking personal fulfillment and a balanced lifestyle through consumption choices.

B. Omnichannel Shopping Preferences

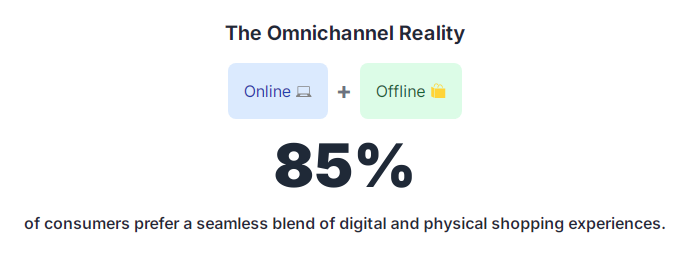

Integration of Online and Offline Experiences: The integration of online and offline shopping channels stands as a defining characteristic of China’s contemporary consumer landscape. Consumers no longer view these channels as distinct but rather as complementary components of a unified shopping journey. A substantial 85% of Chinese consumers now express a preference for a combination of physical stores and digital platforms for their shopping needs, indicating a seamless blending of retail experiences. This preference necessitates that businesses adopt comprehensive omnichannel strategies to meet consumers wherever they choose to engage.

Growth of O2O Services: The rapid rise of Online-to-Offline (O2O) services, particularly instant retail, is fundamentally reshaping the retail ecosystem by bridging the gap between digital convenience and immediate physical fulfillment. Consumers can now effortlessly order a wide array of goods online—ranging from daily groceries and consumer electronics to even luxury items—and expect them to be delivered to their doorstep within a matter of hours. The penetration rate of third-party home delivery service platforms, a key enabler of O2O, significantly increased from 49% in 2023 to 59% in 2024. Concurrently, the user conversion rate on these platforms also saw a notable rise, from 59% to 63%. This growth underscores the increasing reliance of consumers on these services for immediate satisfaction and convenience, making efficient logistics and rapid delivery critical competitive differentiators in the market.

C. Generational Deep Dive: Gen Z and the Silver Economy

Understanding the distinct behaviors of different generational cohorts is crucial for targeted marketing in China.

Gen Z

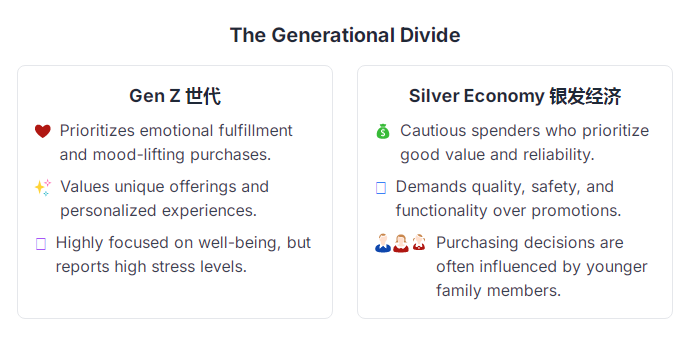

Spending Habits and Priorities: Generation Z consumers in China, typically in the exploratory phase of their careers, generally possess a lower annual disposable household income compared to older generations, primarily due to less work experience and their single status. Despite these financial constraints, a significant 43% of Gen Z consumers have increased their spending on food and beverages, explicitly to uplift their mood and enhance accessibility to these products. This generation places a high priority on physical exercise, weight management, and skin health, reflecting a strong focus on personal well-being. Notably, Gen Z reports the least satisfaction with their mental health, with stress and anxiety being their top concerns, followed by a pronounced desire for mood improvement.

Value and Individuality: Gen Z consumers are discerning about value, but their definition extends beyond mere price. They highly value product aftercare, unique offerings, and leading preferred brands, reflecting a desire for good value for money that incorporates quality and brand experience. Individuality is also a crucial aspect of their consumption, particularly in food choices, where the ability to personalize options to align with their taste, style, and values is highly important. This emphasis on personalization and unique experiences presents opportunities for brands to develop products that cater to their specific preferences and emotional needs.

Optimism vs. Reality: Despite facing significant challenges such as high youth unemployment and lower income growth expectations, urban Gen Z remains among the most optimistic consumer groups in China. This cohort expresses a clear intention to increase their daily spending by 2.6% in 2025, a decision primarily driven by their pursuit of a higher quality of life and personal fulfillment. This dichotomy highlights a resilient mindset where, despite external pressures, the desire for personal well-being and enjoyable experiences continues to drive spending.

Silver Economy

Rapid Growth in Online Consumption: Elderly shoppers represent the fastest-growing segment of online consumers in China, signaling a significant demographic shift in digital engagement. China’s “silver economy,” encompassing products and services for older adults, is projected for substantial expansion, growing from 7 trillion yuan ($974 billion) in 2024 to an estimated 30 trillion yuan by 2035, at which point it is expected to account for 10% of the country’s GDP. This growth is evident in the performance of major e-commerce platforms, with JD.com reporting that senior consumer spending doubled between January and September 2024.

Digital Engagement: A substantial 329 million older adults are now active internet users in China, demonstrating a remarkable embrace of digital platforms. These users spend an average of 129 hours per month online, actively engaging with short videos, e-commerce platforms, and instant messaging, collectively signaling a strong and increasing rise in digital consumption within this demographic. This level of engagement dispels previous notions of a digital divide among seniors and highlights their growing comfort and reliance on online services.

Unique Purchasing Drivers: While increasingly active online, Chinese seniors often maintain a preference for face-to-face interactions when it comes to building trust and ensuring product assurance, particularly for essential goods. They are generally cautious spenders, prioritizing good value for money over the cheapest options, a habit deeply rooted in past experiences of frugality. For this demographic, quality, safety, and reliability are paramount, especially for food products, with 84% of Tier 1 and Tier 2 city respondents reporting an upgrade to higher-quality products and services. Functionality is favored over promotional offers, with a clear preference for factual information and solid evidence supporting product claims.

Influence of Younger Generations: A significant dynamic within the silver economy is the influence of younger generations on senior purchasing behavior. Over half of online purchases for senior-related products are driven by younger individuals, primarily those aged 26-45. This suggests that younger family members frequently handle online purchases for seniors or significantly impact their decision-making processes, bridging any remaining digital gaps. This intergenerational influence means that marketing strategies targeting seniors must also consider the preferences and purchasing habits of their younger family members.

V. Regulatory Landscape and Challenges for Foreign Companies

China’s digital economy operates under a comprehensive and evolving regulatory framework that presents both opportunities and significant compliance challenges, particularly for foreign companies.

A. Data Security and Privacy Regulations

China has rapidly developed one of the world’s most extensive and fast-evolving data governance regimes, characterized by stringent data protection laws. The Cybersecurity Law (CSL) enacted in 2017, the Data Security Law (DSL) effective since September 2021, and the Personal Information Protection Law (PIPL) enacted in November 2021, collectively establish a robust framework for handling digital data. These laws are not merely about privacy; they are strategically aimed at asserting state sovereignty, enhancing national security, and projecting global power.

The PIPL, China’s first comprehensive personal data law, mandates explicit user consent before collecting, using, or disclosing any personal data and critically applies extraterritorially to foreign companies handling Chinese citizens’ data. This means any firm targeting Chinese consumers, even from abroad, must adhere to Beijing’s rules. The DSL complements the PIPL by establishing comprehensive security measures for data processing across its entire lifecycle, from collection to storage and disposal.

A key requirement is local data storage: data generated by Chinese citizens within China is generally expected to be kept within the country, with exceptions for business purposes. Before any data transfer, users must be informed about the type, extent, purpose, and recipient of the data, and provide explicit agreement. For minors, guardian consent is necessary.

As of 2025, China is accelerating the exploration of updated pathways to ensure the safe and orderly flow of data across borders, with gradual easing of restrictions. The Regulations on Promoting and Regulating the Cross-Border Data Flow (“Cross-Border Data Regulations”) provide clear guidelines on three routes for cross-border data transfer as outlined in the PIPL: Security Assessment by the Cyberspace Administration of China (CAC), Personal Information Protection Certification, and Standard Contract filings. The CAC considers necessity and proportionality in these assessments. Furthermore, Free Trade Zones (FTZs) are permitted to develop “negative lists” for cross-border data transfer, exempting data not on these lists from the general framework. FTZs in Tianjin, Beijing, Hainan, Shanghai, and Zhejiang have already released such lists covering 17 industry sectors, with further expansion expected. The Beijing FTZ’s negative list, published in August 2024, notably covers the automobile and life sciences industries.

These measures aim to provide more detailed guidance for data and cybersecurity compliance, enhancing China’s data protection and cybersecurity governance and enforcement efforts. For foreign companies, this necessitates a thorough re-evaluation of data management practices and marketing tools to ensure alignment with these regulations, potentially limiting the use of some international software solutions.

B. Content Censorship and Advertising Regulations

China maintains one of the strictest censorship regimes globally, mandated by the Chinese Communist Party (CCP), primarily for political reasons such as curtailing opposition and censoring events unfavorable to the Party. This censorship extends to all media capable of reaching a wide audience, including television, print, radio, film, text messaging, instant messaging, video games, literature, and the Internet. The government asserts its legal right to control internet content within its territory, claiming it does not infringe on citizens’ free speech.

For the domestic internet community, the Propaganda Department issues editorial guidelines, and social media platforms conduct self-censorship, automatically filtering sensitive content. Users are required to register with their real names, and censors review posts. For foreign websites, the “Great Firewall” blocks access to particular websites with sensitive content by blocking their IP addresses.

Advertising laws in China are particularly stringent regarding content. Advertisements are prohibited from containing anything related to violence, pornography, terror, gambling, superstitious beliefs, or obscenity. Specific restrictions apply to alcohol advertisements, which cannot depict dangerous activities like driving under the influence or imply relaxation, reduced anxiety, or improved physical strength. The use of images or names referring to State organizations or their workers is forbidden, as is content that attacks the dignity or reveals secrets of the Chinese State. Discriminatory content based on race, religion, or gender is also prohibited, as is any information that endangers people’s safety or property. Furthermore, absolute terms like “better,” “higher quality,” or “number 1 in the world” are generally not allowed, and all numerical or statistical data presented in advertisements must be accurate and cite their source.

The revised Anti-Unfair Competition Law (AUCL) of 2025 has expanded its extraterritorial reach, meaning foreign companies can be subject to its provisions if their conduct outside China disrupts the Chinese market or harms the interests of Chinese operators or consumers. This law now explicitly regulates the unauthorized use of well-known trademarks as search keywords, even if not visible in search results, and strengthens prohibitions against fabricating or spreading false or misleading information that damages competitors’ commercial or product reputations. This includes instructing third parties or “water armies” to engage in such conduct, reflecting enforcement trends in digital marketing and influencer spaces. The AUCL also introduces prohibitions against unauthorized data acquisition, platform rule abuse (e.g., fake transactions, fake reviews), and algorithmic or technical manipulation that interferes with competitors’ online products or services. Violations can lead to substantial fines, up to RMB 5 million, with personal liability for key individuals in certain cases.

For foreign brands, this complex regulatory environment necessitates thorough market research and a deep understanding of local dynamics before implementing digital marketing strategies. Successful foreign brands like Apple and KFC have demonstrated the importance of cultural localization, tailoring products, services, and marketing approaches to Chinese tastes and values, and establishing strong local partnerships. Conversely, companies like eBay and Amazon faced significant challenges when failing to adapt sufficiently to local competition and consumer preferences. The geopolitical landscape further complicates matters, with escalating regulatory scrutiny from Western countries impacting Chinese AI firms and potentially leading to reciprocal actions. This environment demands that foreign companies not only comply with China’s strict laws but also strategically adapt their operations and marketing to the unique cultural and competitive nuances of the market.

VI. Conclusions and Strategic Implications

The analysis of China’s online market reveals a landscape of immense scale, rapid innovation, and intricate complexities. The digital economy continues its robust expansion, with digital advertising, digital media, social commerce, e-commerce, and instant retail all demonstrating significant growth trajectories. This growth is fundamentally propelled by China’s pervasive mobile internet penetration, establishing a “mobile-first, video-centric, social-driven” imperative for market participants. Success in this environment hinges on more than just a mobile-optimized presence; it demands substantial investment in short-video content, interactive ad formats, and seamless social commerce experiences integrated directly within super-app ecosystems like WeChat and Douyin. Brands must prioritize creating immersive, visually rich content that encourages direct engagement and immediate conversion within these platforms.

The social commerce sector, particularly exemplified by Douyin’s evolution, is maturing beyond its initial influencer-centric model. The notable shift towards shelf-based shopping and merchant self-broadcasts on platforms like Douyin indicates a move towards more intent-driven purchasing and a reduced reliance on expensive top-tier influencers. This development suggests that while influencer marketing remains relevant, brands must increasingly invest in and optimize their own official stores and conduct consistent, high-quality merchant self-broadcasts to capture both “interest” (discovery via content) and “intent” (search and direct purchase via mall features). This diversification can lead to more sustainable and cost-effective sales channels.

Artificial intelligence is emerging as a powerful efficiency multiplier within China’s digital marketing ecosystem. While its direct application in creative marketing campaigns is still developing, its immediate impact is seen in enhancing back-end efficiencies, data-driven decision-making, and operational streamlining. The emergence of cost-efficient domestic AI models, such as DeepSeek AI, is democratizing access to advanced AI capabilities, compelling major tech giants to lower their service rates. This will make sophisticated AI tools accessible to a broader range of businesses, potentially leveling the competitive playing field and making AI-powered optimization a baseline expectation rather than a premium advantage. Businesses should prioritize integrating AI for operational efficiencies within their marketing departments, focusing on areas like automated ad placement, predictive analytics for user insights, and AI-assisted content generation.

Furthermore, the data challenges the conventional wisdom that traditional media is obsolete in the digital age. The respectable return on investment demonstrated by Linear TV and Print, sometimes even outperforming digital channels like Search, underscores the enduring value of these mediums, particularly for brand building and broad reach. This implies that marketers in China should avoid a purely digital-centric approach. A balanced, multi-channel strategy that leverages the unique strengths of both digital (for precision targeting, engagement, and direct conversion) and traditional media (for broad brand awareness, trust, and credibility) is crucial for optimal return on investment.

Consumer behavior is marked by a shift towards purpose-driven consumption, prioritizing value, quality, and transparency amidst economic uncertainties. The demand for convenience and immediate gratification, particularly through instant retail and O2O services, is reshaping fulfillment expectations. Generational nuances are critical: Gen Z seeks emotional fulfillment and individuality despite financial constraints, while the burgeoning “silver economy” exhibits increasing digital engagement but maintains a cautious, value-driven approach, often influenced by younger family members. Brands must tailor their offerings and messaging to these distinct generational values, focusing on authenticity, transparency, and seamless omnichannel experiences.

Finally, navigating China’s complex and evolving regulatory landscape, especially concerning data security, privacy, and content censorship, remains paramount. The extraterritorial reach of Chinese laws necessitates meticulous compliance for all foreign companies operating in or impacting the Chinese market. Strategic adaptation, cultural localization, and a deep understanding of local compliance requirements are not merely advantageous but essential for sustained success in this unique and highly competitive digital environment.