Navigating the New China: A Strategic Guide to High-Value Opportunities for Western Enterprises

- On December 12, 2025

- china market, opportunity china

1. The New Reality: Redefining “Opportunity” in China’s Evolving Market

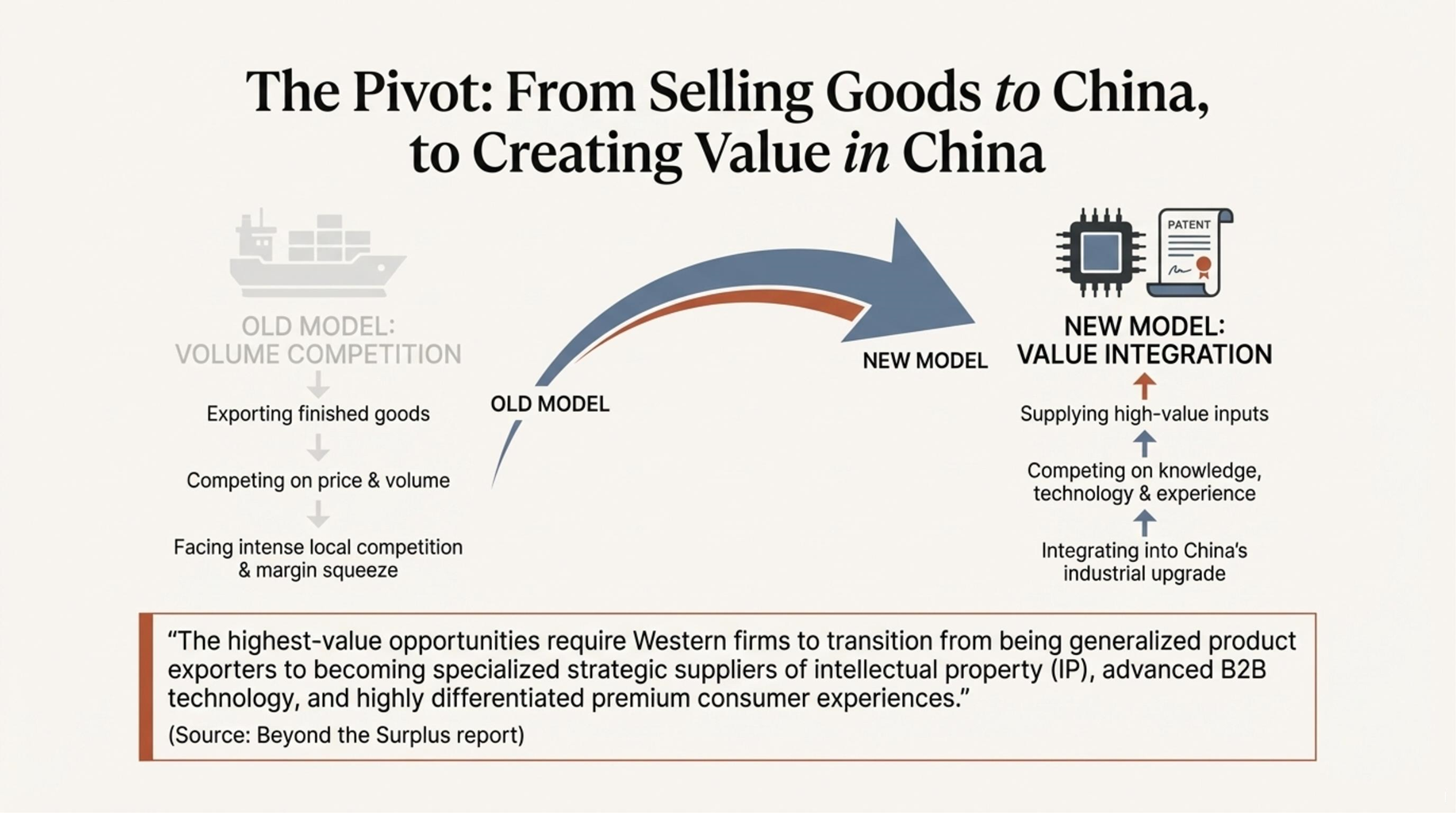

For Western business leaders, traditional models of competing in China on sheer volume are now obsolete, challenged by a formidable new class of sophisticated and agile local competitors. The landscape has fundamentally transformed. This report’s central thesis is that profitable growth is no longer a function of market entry, but of strategic discipline. The imperative for Western enterprises is to execute a decisive pivot from being general goods exporters to becoming specialized suppliers of high-value services, proprietary technology, and premium consumer experiences that align with China’s next phase of economic development. This is not merely an opportunity; it is the only viable path to market leadership.

1.1. Beyond the Goods Surplus: A Misleading Metric

China’s goods trade surplus, which has surpassed one trillion U.S. dollars, is a powerful indicator of its unparalleled efficiency in mass-scale manufacturing. However, for Western firms, this metric is often misleading. It primarily reflects China’s entrenched dominance in production, not the most lucrative areas for market entry or investment.

A more telling narrative is unfolding in the services sector. While the goods surplus captures global attention, China’s services trade volume has also eclipsed the $1 trillion mark. This market is demonstrating dynamic growth, particularly in knowledge-intensive areas. This dichotomy—a massive goods surplus reflecting China’s production strengths and a rapidly growing services import market reflecting its demand for external expertise—frames the new frontier of opportunity. Profitability now resides in bridging China’s knowledge and service deficits, not in competing head-to-head on manufactured goods.

1.2. The Profitability Paradox: Pockets of Resilience Amidst Widespread Pressure

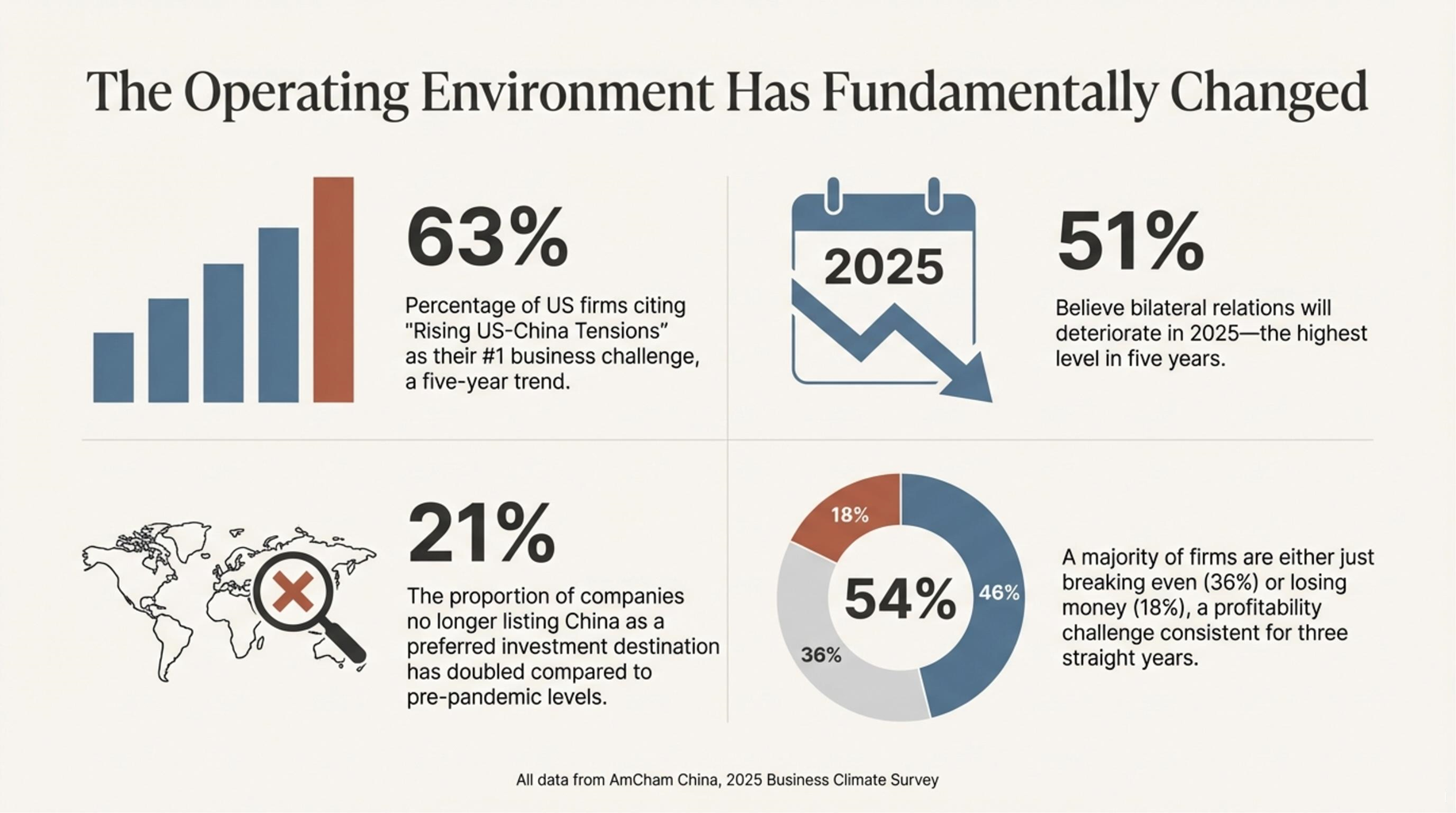

The current business climate presents a clear paradox. According to the 2025 AmCham China Business Climate Survey, overall profitability for U.S. firms has been under pressure for the third consecutive year. Just 46% of surveyed companies expected to be profitable in 2024, while another 36% anticipated only breaking even. This challenging environment is most acute in the general consumer and services sectors, where intense local competition has squeezed margins.

However, this aggregate data masks crucial pockets of resilience. The same survey reveals that firms in the Technology & R&D and Resources & Industrial sectors reported a significantly higher degree of profitability. This indicates that while the broader market is challenging, demand for specialized, high-value industrial inputs and advanced technology remains robust and offers a more defensible path to commercial success.

1.3. The New Strategic Imperative: “In-China, For-China/For-Global”

Sustainable success in China now demands a fundamental shift away from a simple export model. The new imperative is to adopt a deeply localized “In-China, For-China/For-Global” strategy, leveraging Foreign Direct Investment (FDI) to build high-tech innovation and service centers within the country’s ecosystem.

This approach is best described by the German Chamber of Commerce as “Localization 3.0″—a fully integrated value chain with local R&D, manufacturing, and sales. It is a model of being “Chinese-engineered, Chinese-driven and Chinese-powered.” This level of deep integration moves a company from being a foreign entity operating in China to becoming an indispensable part of the local industrial and consumer landscape. This new strategic reality is not occurring in a vacuum; it is being shaped by clear, top-down policy drivers that signal where future growth lies.

2. Decoding the Policy Landscape: Aligning Strategy with China’s National Priorities

For any Western enterprise, understanding China’s top-level policy mandates is of paramount strategic importance. These policies should not be viewed as obstacles but as clear signposts that highlight government-supported growth sectors, point toward areas of cultivated future demand, and provide a roadmap for aligning corporate strategy with national priorities.

2.1. The “High-Quality Development” Mandate

China’s economic focus has officially shifted from the sheer pursuit of GDP growth to a more nuanced emphasis on “High-Quality Development.” This national strategy is anchored in the policy of “adhering to expanding domestic demand as the strategic base.” This is not a call for more of the same, but a push to upgrade the quality and diversity of consumption. The state explicitly supports the promotion of “International Premium Products”, creating a sanctioned pathway for high-end Western brands to differentiate themselves.

Critically, the government now emphasizes both Gross Domestic Product (GDP) and Gross National Income (GNI), signaling a structural shift in demand toward services and experiences that improve citizens’ quality of life. This top-down focus on GNI is the primary policy driver creating the structural demand for the wellness, high-level healthcare, and eldercare solutions that constitute the emerging “silver economy.”

2.2. The Three Pillars of Modernization: Green, Digital, and AI

China’s leadership has articulated a clear strategic imperative to deepen international cooperation in three key technology sectors: Green, Digital, and Artificial Intelligence (AI). Companies whose products and services directly align with these pillars are positioned to benefit from both organic market demand and direct state-level policy support. Opportunities are particularly strong for firms in the green technology sector, such as suppliers of advanced components for renewable energy infrastructure and solutions that enable decarbonization. Similarly, the digital economy requires developers of industrial Internet of Things (IIoT) software, specialized enterprise solutions, and cybersecurity compliance tools, while the AI pillar creates demand for providers of advanced algorithms and smart-vehicle systems that contribute to industrial modernization.

2.3. Catalyst for FDI: The Landmark Opening of Manufacturing

A landmark policy change, effective November 1, 2024, has seen the complete removal of all remaining foreign investment restrictions in the manufacturing sector. This move eliminates previous barriers in industries such as publishing and the processing of traditional Chinese medicine. This policy is more than a regulatory update; it is a formal invitation for Western multinational corporations to prioritize high-tech FDI. Critically, it represents a time-sensitive strategic window. It allows Western firms to establish a defensible, high-tech manufacturing footprint and integrate into local value chains before domestic competitors fully dominate the next generation of industrial technology.

These policy directives are not abstract goals; they are actively shaping the commercial landscape, creating tangible and government-endorsed opportunities in the key sectors we will now explore.

3. High-Potential Sectors: Where to Invest and Compete

The most compelling opportunities for Western firms exist at the intersection of Chinese demand and domestic capability gaps. Where the market’s appetite for superior quality, specialized knowledge, or unique experiences outstrips local supply, high-value openings emerge. This section details three such high-growth domains, providing a clear roadmap for investment and competition.

3.1. The Knowledge Economy: Services, IP, and Digital Solutions

China’s transition to a knowledge-based economy is fueling intense demand for sophisticated foreign inputs. Imports of Knowledge-Intensive Services (KIS) grew by 5.4% overall, a clear indicator that Chinese enterprises are willing to pay a premium for technological superiority and specialized expertise. This is most evident in the 8.7% year-over-year growth in payments for Intellectual Property (IP) Usage Fees, confirming that Chinese firms are actively licensing Western patents and royalties to accelerate their own industrial upgrades.

The financial services sector also presents a significant opportunity, where reforms now permit 100% foreign ownership of banking and insurance subsidiaries, inviting new players and allowing existing ones to consolidate control.

The following table maps key growth areas in service imports to the corresponding opportunities for Western firms.

| Service Category (Import Growth) | YOY Import Growth Rate (%) | Target Western Opportunity |

| Personal, Culture, and Entertainment | 29.5% | High-end content licensing, media distribution, experience design (B2C) |

| Travel Services | 29.3% | Premium hospitality, specialized business/medical tourism services (B2C/B2B) |

| Intellectual Property Usage Fees | 8.7% | Advanced manufacturing patents, R&D collaboration royalties (B2B) |

| Telecom, Computer, Information Services | Strong Growth | Cloud/SaaS solutions, specialized enterprise software, cybersecurity compliance (B2B) |

| Financial Services & Insurance | High Demand | Green finance, specialized investment products, full ownership of local subsidiaries (B2B/B2C) |

3.2. The Industrial Upgrade: Advanced Manufacturing and Green Technology

In line with the “Made in China 2025” initiative, China’s manufacturing sector is undergoing a profound transformation toward high-value, intelligent, and sustainable production. This creates significant demand for foreign technology and investment in sectors such as automotive, robotics, power and energy storage, and biomedicals.

Leading German firms offer a clear blueprint for this strategy in action:

- Volkswagen has established a full-process R&D and testing center in Hefei, its first outside of Germany.

- Siemens has launched a new MRI production base in Shenzhen.

- Bosch has committed to a $1.4 billion smart-vehicle project in Suzhou.

Furthermore, collaboration is increasing, with Western firms like Audi integrating Chinese technology, such as Huawei’s intelligent driving system, into their new models. This demonstrates a shift from pure competition to strategic partnership and deep integration into China’s high-tech ecosystem.

3.3. The Premium Consumer: Experience, Wellness, and E-Commerce

While the mass-market consumer space is fiercely competitive, the premium segment offers significant growth. Success here is increasingly driven by a sophisticated presence on e-commerce platforms like Tmall, JD.com, and Douyin, which serve as the primary gateway to China’s consumer landscape. Key FDI areas within the Fast-Moving Consumer Goods (FMCG) sector include food and beverages (especially supplements), personal care, pet care, and cosmetics.

Beyond traditional retail, China’s aging population is creating a vast “silver economy.” This demographic shift is driving structural demand for foreign healthcare products, high-level medical treatments, and innovative eldercare solutions such as hospice care, a market that is currently underserved by domestic providers. Capturing these opportunities, however, requires a clear-eyed strategy for navigating the formidable competitive and regulatory challenges that define the market.

4. The Strategic Playbook: Navigating a Formidable Competitive and Regulatory Environment

The Chinese market presents a dual reality: it is rich with high-value opportunities but remains one of the world’s most formidable operating environments. Success requires a proactive playbook designed to mitigate the intense pressures of both fierce local competition and a complex, ever-evolving regulatory landscape. Success requires a tripartite strategy: countering domestic rivals through differentiation, rebuilding trust through deep integration, and leveraging regulatory complexity as a competitive moat.

4.1. Countering the Squeeze: The Imperative of Differentiation and Localization

The rise of highly sophisticated and agile domestic competitors is one of the most significant challenges facing Western firms. In the electric vehicle market, for example, nimble domestic players like BYD and NIO have rapidly eroded the market share of established international firms like Tesla. The 2025 AmCham survey reinforces this reality, with competition from Chinese companies ranking as the second-biggest business challenge, cited by 39% of U.S. firms.

The only viable strategic response is a relentless focus on differentiation and deep localization. Competing on price is a losing battle. Instead, firms must justify a premium market position by emphasizing non-price factors: superior and demonstrable R&D, unique brand heritage, alignment with global sustainability standards, and unparalleled quality.

4.2. Navigating the Confidence Gap: From “De-risking” to Deep Integration

A persistent paradox defines the current business climate. On one hand, China is pursuing policy openings, such as the full liberalization of the manufacturing sector. On the other, geopolitical tensions are eroding investor confidence, with the 2025 AmCham survey showing that 51% of U.S. companies expect bilateral relations to deteriorate. This confidence gap is particularly acute in the Technology & R&D sector, where 49% of firms report feeling they are treated unfairly compared to local companies.

The essential strategy to bridge this gap and build operational resilience is deep integration and the formation of local partnerships. The trend of German automakers collaborating with Chinese technology firms is a prime example of this strategy in practice. By embedding their operations and aligning with local partners, companies can better navigate uncertainty and demonstrate long-term commitment, insulating themselves from geopolitical volatility.

4.3. Compliance as a Competitive Moat

The top regulatory challenges cited by U.S. firms include inconsistent regulatory interpretation, unclear laws, and ever-present compliance risks. While these hurdles are significant, they also present a strategic opportunity. Instead of viewing the high cost of compliance—particularly in complex areas like data localization and cybersecurity—as a mere operational burden, leading companies should treat it as the foundation of a “competitive moat.”

Making the substantial investment required to achieve full regulatory adherence creates a high barrier to entry. This secures market access for large, committed firms with the resources to navigate the system effectively, while simultaneously deterring smaller or less-resourced competitors. In this sense, robust compliance becomes a strategic asset that underpins long-term market stability. Thriving in this complex environment requires a new strategic framework that turns these challenges into sources of competitive advantage.

5. Conclusion: A Framework for Success in China’s Next Chapter

The narrative of opportunity in China has fundamentally shifted. Success is no longer a function of mass-market entry but the result of establishing a disciplined, differentiated enterprise focused on three core pillars: Knowledge, Quality, and Deep Integration. The path forward requires a clear-eyed assessment of where Western firms hold a true competitive advantage and a willingness to commit to a deeply localized, high-value operating model.

5.1. A Strategic Framework for Capturing Value

This report’s analysis distills into a four-pillar strategic framework for Western enterprises navigating China’s next chapter:

- Shift from Product Sales to Intangible Asset Monetization: Focus on IP, patents, and proprietary software as primary revenue streams. Capitalize on high-margin, lower-risk licensing agreements that leverage core technological advantages without requiring direct competition in commoditized product markets.

- Commit to Localized High-Tech FDI: Capitalize on the full opening of the manufacturing sector to build local R&D and production centers for high-specification components. Integrate deeply into China’s industrial upgrade by becoming a critical supplier within the domestic ecosystem.

- Elevate Compliance to a Strategic Asset: Treat complex regulatory adherence not as a burden, but as a competitive advantage. Invest to build operational resilience and create a high barrier to entry that insulates your market position from less committed competitors.

- Target the Premium Niche: Avoid debilitating price wars by focusing on the high-growth premium experience economy. Leverage superior quality, global brand equity, and unique cultural offerings that domestic firms cannot easily replicate to command a defensible market position.

5.2. Concluding Outlook

Persistent geopolitical and market risks will continue to define the operating environment in China. The challenges are real and require sophisticated, long-term strategic planning. However, for companies willing to adapt their business models, commit to deep localization, and align their strengths with China’s national priorities, the market remains not only vital but also highly rewarding. The competitive landscape is formidable, but it also sharpens innovation and builds resilience. As Bowen Han, Senior Consultant at strategy consultancy Sinolytics, advises:

“If you don’t come to China, China will come to you… so why not come, compete and be prepared.”

Top 5 Frequently Asked Questions (FAQs) on China’s Business Landscape

1. What major recent policy change has China made regarding foreign investment market access, particularly in manufacturing?

China released the 2024 Edition of the Special Management Measures for Foreign Investment Access (Negative List) on September 8, 2024, which reduced the number of restrictive measures from 31 to 29, marking a significant step toward continuous economic opening. Most notably, the 2024 Negative List completely eliminated all remaining restrictions on foreign investment in the manufacturing sector, providing a more open and competitive environment for global investors. This removal includes cancelling previous restrictions on sectors such as publishing and printing (removing the requirement for Chinese corporate control) and the processing of traditional Chinese medicine (TCM) decoction pieces and the production of confidential formulas for proprietary Chinese medicines. This commitment aligns with policy efforts to attract high-tech Foreign Direct Investment (FDI) in areas like high-specification components, smart manufacturing, and green production.

2. What is the number one business challenge reported by US companies operating in China, and how is the outlook for bilateral relations viewed?

For the fifth consecutive year, rising tensions in US-China relations remain the top business challenge cited by foreign firms operating in China, selected by 63% of responding companies in the 2025 survey. The impact of these tensions on business strategy has increased, forcing companies to delay or cancel China investment decisions (22% in 2024) and adjust supply chains by seeking sourcing or assembly outside of China (21% in 2024). Due to factors like the anticipated 2025 US administration change, policy uncertainties, and frequent countermeasures, 51% of respondents expressed concern that bilateral relations may continue to deteriorate in 2025, reaching the highest level of pessimism in the past five years,. Despite this pessimism, 87% of responding companies emphasized that a positive bilateral relationship is crucial or extremely important to their operations in China.

3. Which key sectors are identified as major growth opportunities for foreign investment in China in 2025 and beyond?

Opportunities are concentrated in sectors aligned with China’s “High-Quality Development” mandate, emphasizing knowledge, green, and digital technology:

- Knowledge-Intensive Services (KIS) and IP Licensing: There is significant demand for sophisticated foreign knowledge, Intellectual Property (IP) licensing, specialized consulting, and advanced B2B digital solutions. IP Usage Fees imports grew by 8.7% year-on-year, indicating local enterprises are actively purchasing external Western IP.

- Advanced Industrial Technology and Manufacturing: Following the full opening of the manufacturing sector, foreign investment is targeting high-tech and specialized industrial inputs, including advanced components, industrial automation software, and localized R&D. This includes technologies supporting the “Green” and “Intelligent” upgrade of Chinese manufacturing.

- New Energy and Electric Vehicles (EVs): This sector is a pillar of China’s economic strategy, benefiting from a shift toward sustainable development, government incentives, and the country’s dominance in the global battery supply chain.

- Health and Wellness: Driven by an aging population and rising incomes, demand is strong for healthcare technologies, pharmaceuticals, R&D facilities, specialized medical devices, and digital wellness solutions like fitness and mental health platforms. China has also permitted wholly foreign-owned hospitals in nine major cities.

- Artificial Intelligence (AI) and Machine Learning: Rapid adoption and robust government support are driving growth in AI applications across healthcare, finance, manufacturing, and smart cities. The AI sector is projected to grow significantly from US34.2 billionin 2024 to US154.8 billion by 2030.

4. How are international companies responding to intense competition and geopolitical risks in terms of their investment and supply chain strategies?

Foreign companies are adopting a combination of caution, localization, and strategic repositioning:

- Investment Intent: While nearly half of surveyed companies still rank China among their top three global investment priorities, the willingness to increase investment is constrained by geopolitical concerns and slowing economic growth expectations. Over 40% of responding companies indicated they do not plan to increase investment in 2025.

- Supply Chain Relocation: The proportion of companies that have already started or are considering relocating manufacturing or sourcing outside of China has increased, driven primarily by US-China trade tensions (44%) and rising geopolitical tensions (42%). However, 67% of companies are not considering relocating manufacturing or sourcing outside of China.

- Deep Localization (Localization 3.0): Successful firms are implementing an “In-China, For-China/For-Global” model, embedding R&D, design, and sophisticated production locally to meet Chinese consumer preferences and utilize the country’s innovation base. German firms, for example, are setting up new full-process R&D and testing centers in China to accelerate product development.

- Compliance Investment: Due to complex data regulatory environments (such as PIPL) and technology policies, successful entry into B2B tech markets requires treating rigorous compliance and data localization as a necessary, high-value investment that acts as a barrier to less committed competitors.

5. How does China’s strategic pivot toward “High-Quality Development” fundamentally impact opportunities for Western firms?

The strategic pivot toward “High-Quality Development” and emphasizing Gross National Income (GNI) over solely Gross Domestic Product (GDP) structurally shifts China’s demand toward specialized services and premium experiences. This creates opportunities for Western firms whose core advantages lie in specialized knowledge and brand reputation. The focus shifts away from competing in mass-produced goods (where China maintains immense structural efficiency and a massive surplus,) toward bridging China’s service and knowledge deficits. The highest revenue streams are now found in supplying high-value, non-production related inputs—specifically knowledge, specialized technology, and unique premium consumption experiences (such as high-end hospitality, cultural IP exports, and specialized medical services).