The Perception vs. Reality Gap: A 2026 Strategic Playbook for the Chinese Digital Frontier

- On April 14, 2026

- china marketing, china marketing mistakes

1. The Death of the “Cash Cow” Narrative

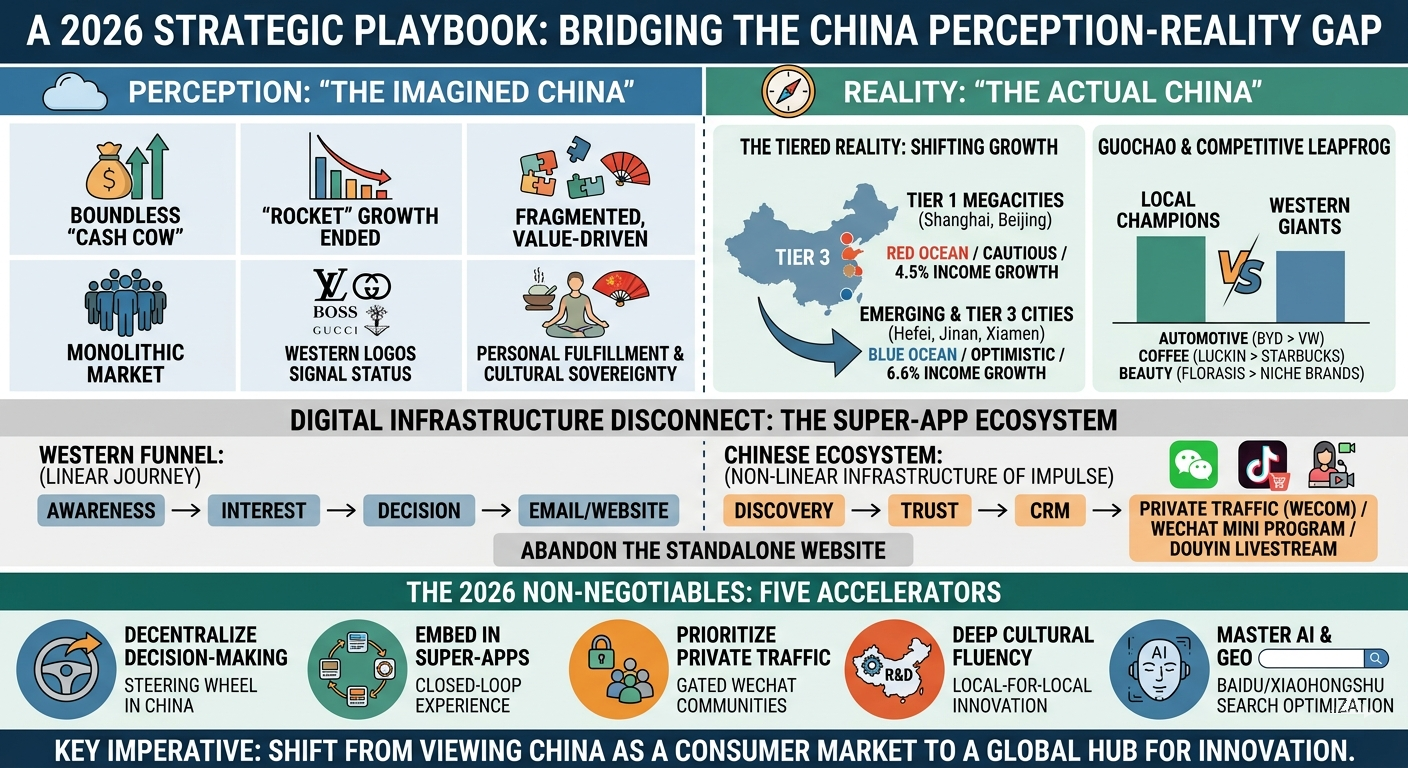

For three decades, Western boardrooms treated the Chinese market as a boundless “cash cow”—a high-growth frontier where global brand equity naturally translated into market dominance. As we navigate 2026, I must be blunt: treating China as a passive revenue source is now a primary driver of corporate insolvency. The era of “rocket-fueled” growth that defined the early 2000s has ended. Success in this “new reality” of single-digit consumption growth is no longer a given; it must be engineered through radical innovation and hyper-localization.

The strategic disconnect lies between an “Imagined China”—a monolithic bloc with an insatiable appetite for Western status—and the “Actual China”, which is fragmented, value-driven, and culturally sovereign. McKinsey’s 2025 survey of 17,000 consumers confirms a seismic shift toward “personal fulfillment.” This is not merely a psychological trend; it is the functional driver behind the “Reverse Migration” to lower-tier cities. Consumers are no longer buying Western logos to signal status; they are seeking quality-of-life upgrades that align with a new, minimalist ideology. To survive, you must deconstruct the geography of Chinese consumption.

2. The Tiered Reality: Beyond the Tier 1 Megacity Obsession

A centralized strategy focused exclusively on Shanghai and Beijing is strategically obsolete. While Tier 1 megacities are trapped in aggressive price wars and “job anxiety” (affecting 36% of urbanites), the true growth engines have moved. You must pivot your capital toward the “Blue Ocean” of Tier 3 and emerging cities.

Economic Trajectories: Tier 1 vs. Emerging Regions (2024-2025)

| Metric | Tier 1 Megacities (Shanghai, Beijing) | Tier 3 & Emerging Cities (Hefei, Jinan, Xiamen, Kunming) |

|---|---|---|

| Income Growth | 4.5% (Urban residents) | 6.6% (Rural/Lower-Tier residents) |

| Consumer Sentiment | Cautious; Asset depreciation | Optimistic; Rising affluence |

| FMCG Growth Contribution | Saturated; Declining share | 80% of total FMCG growth (2025) |

| Strategic Classification | Red Ocean / Price Wars | Blue Ocean / High-Margin Opportunity |

The rise of cities like Hefei, Jinan, Xiamen, and Kunming is fueled by young professionals fleeing the high costs of Tier 1 hubs. This new middle class is rational and quality-seeking. They demand a balance of prestige and affordability. If you fail to localize for these regional hubs—ignoring distinct dialects and cultural nuances—you are ceding the only remaining high-growth segments to local champions.

3. The Brand Equity Crisis: Guochao and the Competitive Leapfrog

The “Guochao” (National Trend) movement has matured into a structural shift in consumer identity, effectively eroding the “Western Premium” default. Today’s youth embrace a minimalist ideology, prioritizing brands that offer “body positivity” and “emotional resonance” over glitzy status symbols.

Local Champions vs. Global Giants: The Performance Gap

- Automotive: Western EV market share collapsed from over 20% in 2023 to 15% in Q3 2025. BYD has leapfrogged Volkswagen by integrating localized autonomous technology at a pace Western R&D cannot match.

- Coffee: Starbucks’ dominance ended as local rivals like Luckin Coffee mastered localized flavor profiles and pricing. In a tacit admission of failure, Starbucks sold a 60% stake in its Chinese business to the local private equity firm Bowi Capital.

- Beauty & Lifestyle: While Western niche brands like Too Faced and Glamglow vanished, “Native Heroes” like Florasis and Neiwai thrived. Neiwai’s focus on body positivity represents a radical departure from traditional Western beauty standards, resonating with the minimalist shift among youth.

The “Steering Wheel” Diagnosis: I have diagnosed the primary driver of MNC failure as a lack of organizational agency; the steering wheel remains in the West while the race is being run in the East. When uncertainty hits, Western HQs “step on the brake,” while the Chinese market demands “stepping on the accelerator.” Decentralization is no longer an option; it is a prerequisite for survival.

4. The Digital Infrastructure Disconnect: Funnels vs. Ecosystems

Western brands routinely attempt to “copy-paste” digital strategies, yet the “Digital Great Wall” renders tools like Google, Email, and Meta irrelevant. In China, “Super-Apps” have constructed an Infrastructure of Impulse—a non-linear buyer journey integrated into the fabric of daily life.

Strategic Comparison: Western vs. Chinese Digital Logic

| Aspect | Western Marketing Imaginary | Chinese Digital Reality |

|---|---|---|

| User Journey | Linear (Awareness → Interest → Decision) | Non-linear (Discovery → Trust → CRM) |

| Digital Driver | Individualistic; Attention-driven | FOMO-driven; Entertainment-integrated |

| Primary CRM | Email Marketing ($36-42 ROI) | Private Traffic / WeCom (Social CRM) |

| Infrastructure | Siloed Apps / Standalone Websites | Integrated Super-Apps (WeChat, Douyin) |

Abandon the standalone website. It is a digital ghost town. Chinese consumers demand a “closed-loop” experience. A luxury skincare brand that bypassed a traditional site for a WeChat Mini Program gamified campaign saw a 46% spike in store visits in one week. Without this integration, your marketing is clunky, inefficient, and invisible to the mobile-first consumer.

5. Platform-Specific Editorial Logic: Douyin and Xiaohongshu (RED)

You must dismantle the assumption that “Douyin is TikTok.” They share DNA but inhabit different universes.

- Douyin (The Consumption Carnival): TikTok is a “Wishing List” for passive entertainment. Douyin is a high-velocity carnival. It utilizes “3-second selling” and Douyin Pay to trigger instant, impulsive conversions. Livestreams here are reality shows optimized for the “Infrastructure of Impulse.”

- Xiaohongshu (The Decision-Making Engine): This is a search-centric discovery engine. Success requires the KFS Model (KOL/KOC + Feed Ads + Search). 60% of users initiate their journey via the search bar, treating the app as a “lifestyle bible.”

The KOC Trust Premium: The Xiaohongshu algorithm rewards “gritty authenticity” over polished production. Crucially, “Saves” (Bookmarks) are the highest indicator of value. A save signals utility and long-term trust, whereas a “Like” is a low-friction metric the algorithm increasingly ignores.

6. From Public Ads to Private Traffic: The ROI of SCRM

As the cost of public acquisition (CAC) skyrockets, you must immure your brand within “Private Traffic”—gated WeChat communities where you own the relationship.

- The Death of Email: Email marketing is functionally dead. It must be replaced by WeCom (WeChat Work) and Mini Program integrations. This allows for real-time, relationship-driven engagement that Western CRM tools cannot replicate.

- Livestreaming as Storytelling: In 2026, livestreaming has evolved from “flash sales” to a critical brand-building tool. Authenticity-driven streams provide 3-4x higher conversion rates than traditional ads by providing real-time service and “grass-planting” (Zhongcao) narratives.

7. Regulatory Sovereignty: Navigating PIPL and Data Compliance

The Personal Information Protection Law (PIPL) is a “hard barrier.” China treats data as a national security asset, and your global data architecture must be dismantled to comply.

PIPL Compliance Framework

| Mandate | Strategic Marketing Impact |

|---|---|

| Explicit Consent | No pre-checked boxes; requires granular, clear opt-ins for every data use. |

| Data Localization | Behavioral and financial datamuststay onshore on local servers. |

| Cross-Border Transfers | Requires security assessments if data affects >100,000 individuals. |

| Penalties | CN¥50 million or 5% of annual revenue; suspension of platform access. |

Conclusion: The “Local-for-Local” Imperative

The 2026 playbook demands a pivot from viewing China as a consumer market to treating it as a global hub for innovation. To bridge the perception-reality gap, you must adopt “Smart Empathy” and follow these five non-negotiables:

- Dismantle Centralized R&D: Adopt “Local-for-Local” innovation to match the speed of local champions.

- Decentralize Decision-Making: Move the “steering wheel” to China. Empower local leadership to accelerate.

- Immure the Brand in Super-Apps: Abandon standalone sites for WeChat Mini Programs and Douyin storefronts.

- Prioritize Private Traffic: Shift budgets from expensive public acquisition to WeChat communities and SCRM.

- Execute Deep Cultural Fluency: Move beyond translation to address the minimalist and Guochao shifts.

You must master Generative Engine Optimization (GEO). This is the response to the optimization of brand content for AI-driven conversational search on Baidu and Xiaohongshu. AI is no longer a tool; it is your co-pilot for navigating the 2026 frontier.