The Death of Apps: Why AI Agents Will Redefine Consumer Entry Points in China and Beyond

- On June 30, 2026

- china app, china social marketing

For the past decade, Western digital marketers looking at China have shared a common consensus: China is the land of the Super App. While the Western internet remained fragmented across individual applications and mobile web browsers, China consolidated into an almighty, all-in-one ecosystem anchored by Tencent’s WeChat.

But as we navigate 2026, a structural tectonic shift is quietly occurring under the surface of China’s internet. The era of the “Search-and-Click” app economy is reaching its twilight. Driven by hyper-fast AI adoption and staggering token volumes from local tech giants, the very layer where consumers interact with brands is being fundamentally re-engineered.

We are transitioning from a Platform Economy to an Intent-Routing Economy. For Western brands operating in or eyeing the Chinese market, understanding this dynamic is no longer about optimizing for a specific platform’s algorithm; it is about survival at the digital point of entry.

1. Executive Insight: The Re-engineering of Distribution Power

In the era of Generative AI, Western corporate strategy remains heavily fixated on infrastructure—who has the most parameters, the biggest clusters, or the lowest latency. However, leading internet strategists and tech executives in China view the battlefield differently. They recognize a fundamental market reality: the structural value of AI scales downward from infrastructure to the consumer interface.

To conceptualize this hierarchy, we can extend a core architectural framework:

Chips (Compute Capacity) -> Models (Commoditized Intelligence) -> Interfaces (Distribution Power)

- Chips and hardware represent raw, foundational infrastructure.

- Large Language Models (LLMs) represent core intelligence, which is rapidly commoditizing. By mid-2026, token pricing among major Chinese model providers has plummeted, rendering raw LLM access a low-margin utility.

- The Interface represents exclusive distribution power.

The ultimate victor in the AI race will not be the company that trains the largest model, but the entity that owns the user’s intent.

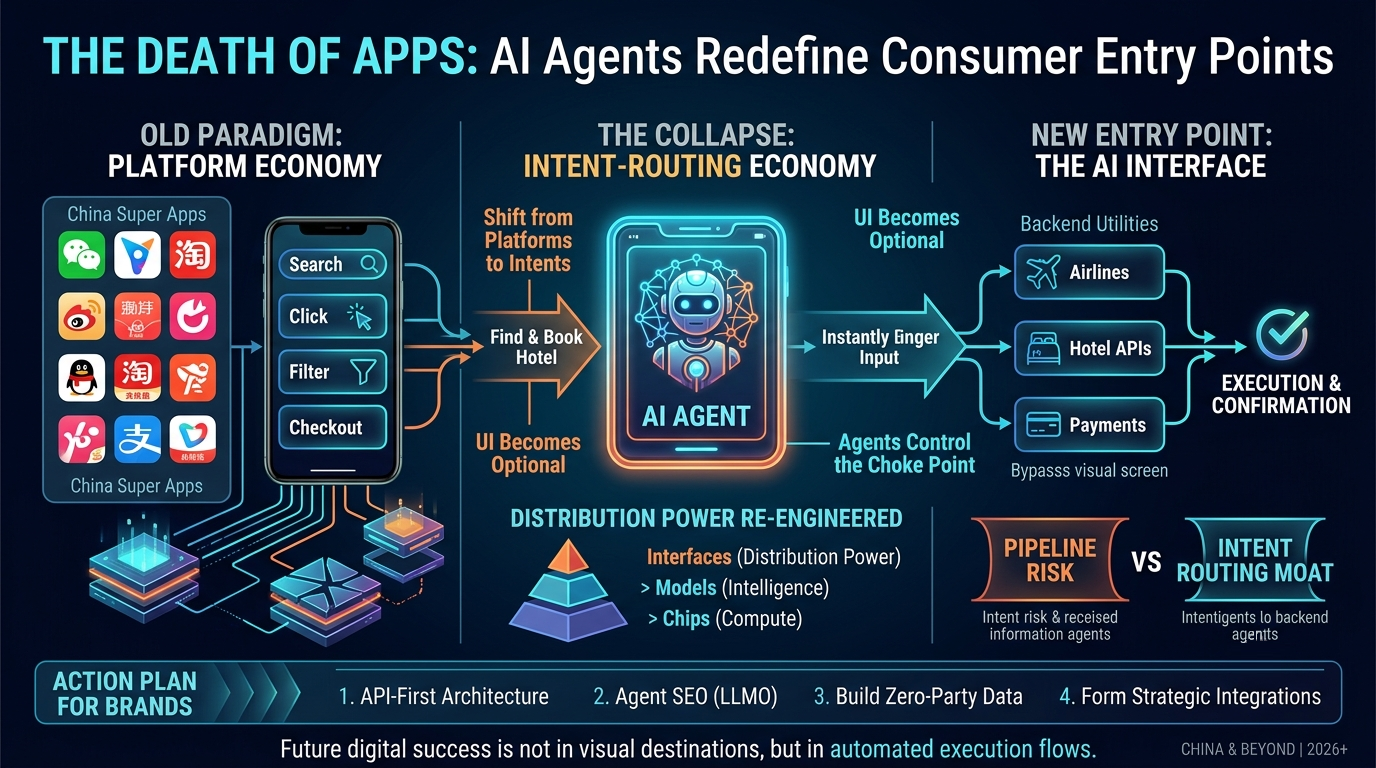

When a consumer no longer opens an app to search, browse, filter, and checkout, but instead dictates a single cross-platform request to an AI Agent, the traditional app ecosystem loses its gatekeeping leverage. The consumer interface is the choke point of the modern digital economy. Whoever controls that interface controls which brands receive traffic, which APIs are executed, and which products are bought.

2. The China Case Study: WeChat as the Prototype of Super-App Power

To understand how AI Agents will dismantle traditional app interfaces, one must look at China’s current baseline: WeChat.

Western marketers often mistake WeChat for a mere messaging app with added features. In reality, WeChat functions as a highly sophisticated, four-layer synthetic operating system built on top of iOS and Android.

+-------------------------------------------------------------+ | WECHAT SUPER-APP OS | +-------------------------------------------------------------+ | 4. PAYMENT LAYER (WeChat Pay - Seamless capital settlement) | +-------------------------------------------------------------+ | 3. MINI-PROGRAM LAYER (Lightweight, zero-install applets) | +-------------------------------------------------------------+ | 2. CONTENT LAYER (Official Accounts, Channels short video) | +-------------------------------------------------------------+ | 1. MESSAGING LAYER (The foundational social identity core) | +-------------------------------------------------------------+

By binding identity (Messaging), information (Content), software (Mini-Programs), and capital settlement (WeChat Pay) into a single, unified interface, WeChat effectively decoupled the consumer from the underlying mobile operating system.

It became the closest real-world example of a closed consumer internet OS. For a Western brand in China, your website did not matter; your standalone iOS app did not matter. Your WeChat Mini-Program was your digital storefront.

Because WeChat unified these four layers so perfectly, it established an absolute monopoly on user attention and consumer intent routing. However, this exact centralization makes the ecosystem highly vulnerable to the next wave of disruption: the collapse of the user interface itself.

3. The Disruption: AI Agents Collapse the UI Layer

The traditional mobile internet—even within WeChat—relies entirely on human navigation through a Graphical User Interface (GUI). Consumers must click, scroll, read, compare, and tap through multiple screens to complete a single task, such as booking a flight or buying a cosmetic product.

AI Agents completely collapse this multi-step journey. Powered by massive leaps in scale—such as ByteDance’s Doubao (which crossed an astounding 180 trillion daily token calls in mid-2026)—and advanced multi-step orchestration, the digital journey has evolved:

- Old Paradigm: Users navigate interfaces.

- New Paradigm: Users express intent; Agents execute workflows.

When a user tells an AI Agent, “Find me a mid-range hotel in Hangzhou close to West Lake for this weekend, book it using my corporate card, and text my itinerary to my spouse,” the agent bypasses the visual interfaces of travel apps entirely. It reads the intent, calls the appropriate APIs, executes the transaction, and returns a natural language confirmation.

The Structural Threat: The traditional UI layer becomes entirely optional. When consumers stop looking at screens filled with brand logos, banner ads, and algorithmic recommendations, the conventional digital marketing funnel—built on impressions, click-through rates (CTR), and visual conversion optimization—completely breaks down.

4. The Three Structural Tensions Facing Brands

This shift from visual platforms to autonomous agents introduces three severe structural tensions within the Chinese digital landscape that Western executives must carefully analyze.

4.1 Supply Explosion vs. Demand Reality

With the proliferation of enterprise AI tools, creating a digital storefront, a localized campaign, or a customer-service Mini-Program has dropped to near-zero marginal cost. WeChat’s rollout of its 2026 AI Mini-Program Growth Plan explicitly democratized cloud compute and LLM capabilities for millions of developers.

However, while the supply of AI-generated applications and tools is exploding exponentially, human attention and consumer intent remain inherently scarce. An abundance of digital creation does not translate to an abundance of consumer usage. Brands that simply use AI to flood the market with more content or more basic apps are shouting into a void.

4.2 Disintermediation of Distribution

In the classic WeChat ecosystem, Mini-Programs rely on explicit user actions: scanning a QR code, searching a precise keyword, or clicking a link shared in a chat.

AI Agents remove manual navigation entirely. As native conversational assistants (like WeChat’s slowly rolling out “Xiao Wei” assistant or ByteDance’s enterprise agents) scale up, distribution shifts from Platforms to Agents.

A brand can no longer buy premium banner placement or top search-result rankings on an e-commerce platform if an agent is autonomously selecting the single best SKU via an API call based on the user’s explicit parameters.

4.3 The Illusion of Data Moats

Many multinational corporations believe their proprietary CRM databases and chat histories within China constitute a defensible data moat. Chinese marketing intelligence reveals this is largely an illusion.

Most historical brand-consumer chat data is highly unstructured, filled with low-signal conversational noise, and heavily protected by strict local privacy frameworks (such as the PIPL). This makes it incredibly difficult to convert into predictive intent models.

Ultimately, behavioral intent records matter far more than communication history. The entity that captures the real-time request at the exact moment a consumer decides to buy holds the actual data moat, not the brand holding a historical log of past transactions.

5. The “Pipeline Risk”: From Platform to Infrastructure

For major digital platforms and brands alike, the rise of the Agent Interface introduces a critical strategic threat: The Pipeline Risk. This is the danger of a premium consumer-facing platform being systematically downgraded from an “entry point” to a mere “execution pipe.”

Consider the standard consumer journeys in China for daily services:

| Industry Sector | Traditional Platform Journey | The AI Agent Paradigm |

| Food Delivery | Open Meituan -> Browse restaurants -> Compare promotions -> Select meal -> Pay | “Order my usual Friday lunch sushi combo.” -> Agent executes backend API call. |

| Ride-Hailing | Open Didi -> Input destination -> Select tier (Express/Premier) -> Call car | “Get me a ride to the airport to catch my 3 PM flight.” -> Agent auto-calls closest vehicle. |

| Boutique Retail | Open Tmall/Xiaohongshu -> Read reviews -> Select size -> Checkout | “Replace my active-retinol night cream with the best deal available.” -> Agent routes to optimal API. |

In this new paradigm, Meituan, Didi, and Tmall lose their direct relationship with the consumer’s eyes. They are no longer lifestyle destinations where users linger; they are transformed into headless utilities—backend infrastructure executing API calls routed to them by the dominant AI Agent interface. When your brand is buried inside an API payload, your capacity to cross-sell, premium-price, or build emotional loyalty evaporates.

6. Strategic Positioning: What Tencent Is Actually Doing

Western observers often look at the massive consumer adoption of ByteDance’s Doubao or the aggressive monetization of independent AI assistants and conclude that Tencent has fallen behind in the AI race. This completely misreads Chinese platform architecture.

Tencent’s strategy with WeChat is defined by deliberate architectural caution, not innovation hesitation.

[ Tencent's Ecosystem Conservation Strategy ]

AI Technology Upgrades (Hunyuan LLM / Cloud Computing)

│

▼

Embedded into Core Infrastructure

│

▼

+───────────────────────────────────────+

| Protects Existing Ad Base (¥100B+) |

| Maintains Stable Mini-Program Core |

| Slow, Native Integration Only |

+───────────────────────────────────────+

Tencent operates a highly lucrative, multi-billion-dollar digital advertising and transactional ecosystem. If they prematurely deploy an unconstrained, all-powerful AI agent at the center of WeChat that completely automates user journeys, they risk cannibalizing their own ad revenues.

If a user never scrolls through a timeline or browses search results, who buys the feed ads?

Consequently, Tencent is methodically embedding its Hunyuan LLM capabilities into the existing architecture—providing AI tools to developers via the 2026 growth plans and testing native assistants like “Xiao Wei” strictly within controlled, native parameters. They are navigating an architectural tightrope: upgrading their infrastructure to prevent disruption by external agents, while preserving the visual, ad-supported environment that generates their current revenue.

7. Global Implications for Western Companies

The ongoing shift in China’s digital architecture offers a predictive looking glass for the rest of the world. However, Western executives must avoid copy-pasting Chinese strategies directly into their global playbooks due to deep structural differences.

7.1 Super-Apps Will Not Repeat in the West

Many Western tech firms dream of building a “Western WeChat.” This is a fundamental misunderstanding of structural market sequencing.

China transitioned directly from desktop to a mobile-first internet when its financial and retail infrastructure was still developing, allowing WeChat to fill an institutional void.

The West, by contrast, features highly mature, deeply fragmented legacy infrastructure: credit cards dominate over unified QR payments; independent web browsers remain highly functional; and strict anti-trust regulations actively prevent a single platform from monopolizing social, payment, and commerce simultaneously. Furthermore, Apple (iOS) and Google (Android) maintain absolute, aggressive gatekeeping control at the mobile operating system level in the West, blocking any third-party app from becoming a true meta-OS.

7.2 The Real Battle is Not App vs. App

Western marketing teams spend millions attempting to win the battle of App vs. App (e.g., optimizing Shopify storefronts versus Amazon positioning). In the AI era, this is the wrong war.

The actual battle is Apps vs. Agents vs. Operating Systems. The ultimate gatekeeper will be whichever layer captures the user’s primary interface. If Apple integrates a highly capable, local AI agent directly into the iOS system level, or if an independent agent app captures dominant consumer trust, individual brand apps and websites will be reduced to background APIs.

7.3 The Next Winners Will Control “Intent Routing”

The historical digital moats—total registered users, volume of raw data collected, or proprietary features—are rapidly depreciating.

The future moat is exclusively Intent Routing: the systemic authority to decide what a consumer does next.

[ THE FUTURE MOAT ]

│

▼

+─────────────────────────+

| Intent Routing |

+─────────────────────────+

│

┌─────────────────────┴─────────────────────┐

▼ ▼

+─────────────────────────────────────+ +─────────────────────────────────────+

| Algorithmic Trust Moat | | Backend Integration |

| Which agent does the consumer trust | | How seamlessly does your brand API |

| to choose their products? | | plug into the routing engine? |

+─────────────────────────────────────+ +─────────────────────────────────────+

8. Strategic Action Plan for Marketing Leaders

To thrive in an economy shifting from “Search-and-Click” to “Request-and-Execute,” Western business owners and marketing directors must completely overhaul their digital strategy.

- Shift from GUI Optimization to API-First Architecture: Stop allocating 100% of your digital budget to visual web design and front-end user interfaces. If your product information, inventory, and checkout systems are not exposed via highly structured, lightning-fast, and AI-readable APIs, autonomous agents will simply skip your brand. Your backend data architecture is your new storefront.

- Optimize for “Agent SEO” (LLMO): Traditional Search Engine Optimization is dying. You must optimize your brand’s digital footprint for Large Language Model Optimization (LLMO). This means ensuring your brand’s technical data, product specifications, customer reviews, and authoritative case studies are deeply ingested by dominant Chinese models (like Hunyuan and Doubao) and global equivalents, ensuring your brand is the preferred recommendation when an agent executes an intent-routing query.

- Build Direct, Zero-Party Data Channels: Because platforms risk becoming mere execution pipelines, you must establish direct, unmediated relationships with your highest-value consumers. Use high-utility, specialized AI agents of your own that provide genuine, differentiated value to consumers, bypassing third-party aggregators to capture unfiltered intent data directly.

- Audit Your Pipeline Risk: Analyze your current revenue lines in China and globally. What percentage of your sales relies on consumers manually browsing a marketplace or clicking a display ad? If that percentage is high, your revenue is highly exposed to pipeline downgrades. Begin building strategic integrations directly with emerging agent interfaces to ensure you are the native, default provider in your category.

The consumer internet is no longer just a collection of digital destinations. It has transformed into an active, automated grid of execution. Brands that continue to build beautiful, isolated digital islands will find themselves completely invisible to the autonomous agents directing the future flow of commerce.